In recent years, card payments have become increasingly popular in Ukraine, as well as globally. In particular, due to its convenience, security and ease of use. In addition, our country is planning to introduce the e-hryvnia as part of its efforts to embrace innovation. However, neither the e-hryvnia or card payments can completely replace cash, but will only be a supplement to it.

Cash remains an important payment instrument. According to the National Bank of Ukraine, as of 1 April, there was UAH 780.3 billion in cash circulation in Ukraine, which is UAH 16 billion, or 2.1%, more than at the beginning of 2024 (UAH 764.4 billion).

In this article, Alla Kyrhyzova, Banking Development Manager at RENOME SMART, explains how to change the usual approach to cash collection and processing.

Transformation of the cash collection process

In today’s Ukrainian realities, where stability and transparency of financial flows are key to successful business, changing the approach to cash management is becoming increasingly important.

This process involves the implementation of technological solutions and software that will ensure a continuous cash processing process and optimise each stage of cash handling. In particular, the function of administering and controlling the company’s cash.

Simply put, it is not about any part of it, but the entire cash flow cycle, where the starting point is the ADM network.

Alla Kyrhyzova

Banking Development Manager

“We offer a financial model – comprehensive processing of large volumes of cash, which will help cash-in-transit companies and banks become more flexible to the needs of their customers. And at the same time, they will be more economical with their own resources.

Cash collection using ADM will allow us to manage costs more efficiently, ensure the required level of service, increase the profitability of the service itself, while reducing the risks of theft or loss of funds, and increase the transparency and reliability of cash handling,” explains Alla Kyrhyzova.

What goals do we achieve with this new approach?

- Increase efficiency. By depositing revenue centrally, using a network of automated deposit machines and in accordance with its own business processes, the company frees up time and resources for strategic tasks. And CIT companies reduce the number of travels, points of contact and related costs.

- Improving security. A certified ATM-class safe reliably protects cash from theft and fraud, even at night.

- We manage revenue instantly. Once deposited into the ATM, the money becomes available on the customer’s current account in a few minutes.

- We have full 360° control. When we manage to conquer routine processes. Recalculation, accounting, validation, detailed transaction information, automated reporting and analytics – all this makes it easier not only to work with cash, but also to make financial decisions.

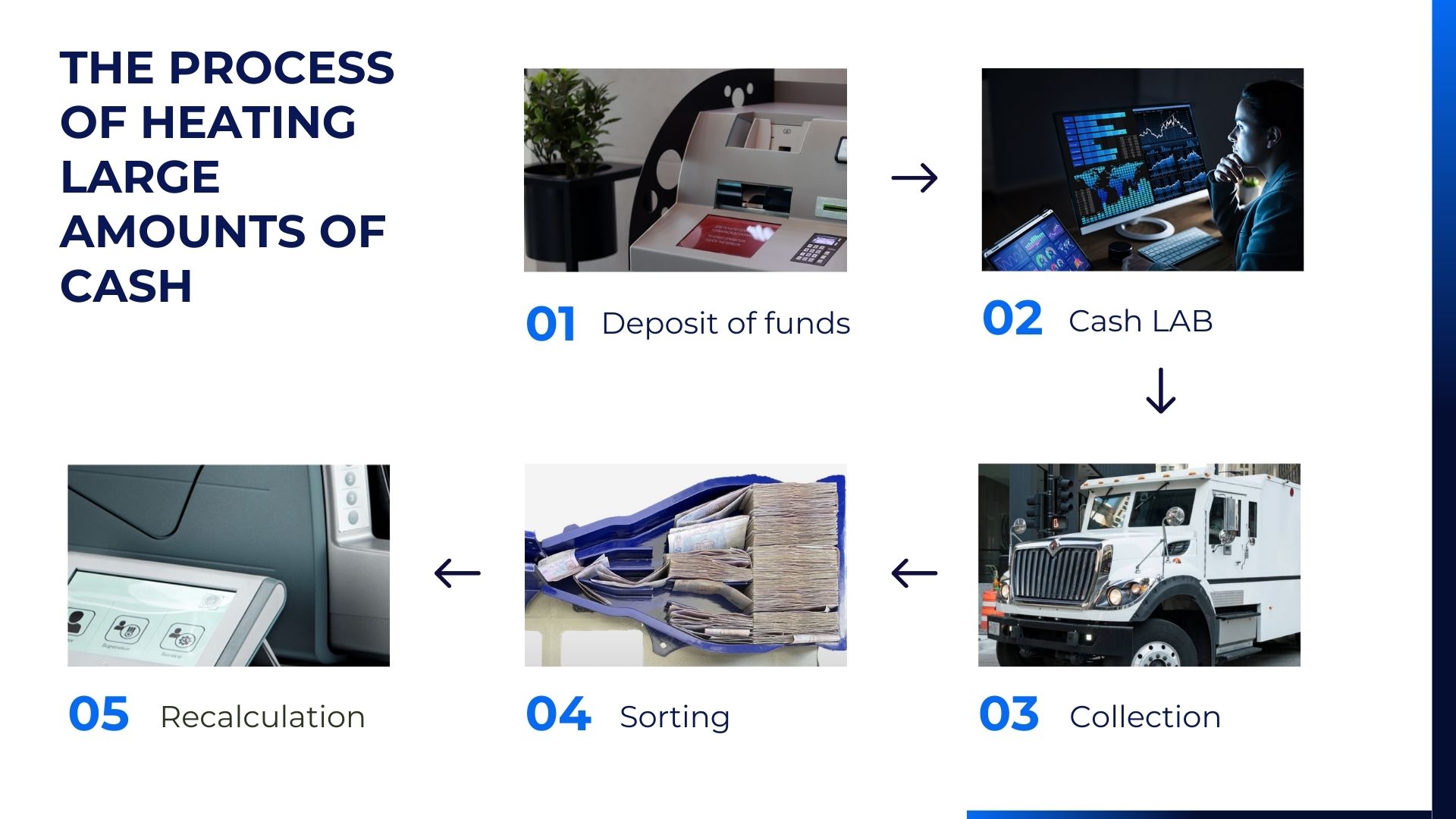

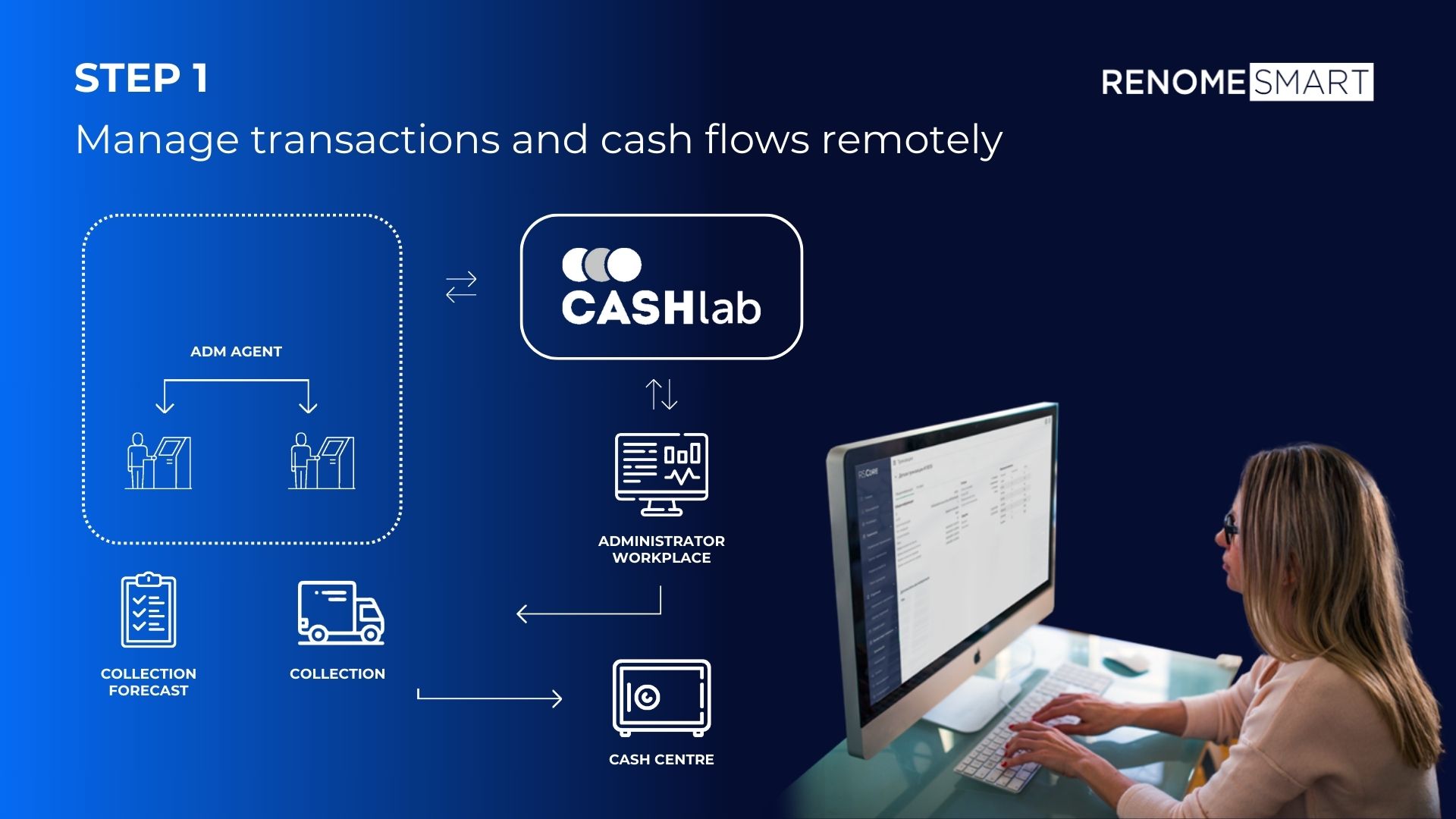

How it works

FIRST STEP – to build a unified network of automated deposit machines for handling large volumes of cash.

The ES 3003 Coin Automated Deposit Machine ━ is an updated model of the ADM that can be supplemented with a coin acceptance module.

It completely replaces the classic cash register for accepting large payments and can simultaneously work with cash of various denominations and currencies. At the same time, it can instantly transfer it to a bank account, record it and safely store it until the arrival of the cash collectors.

The key is that it accepts banknotes in bundles and coins in bulk. It processes and verifies up to 1,200 banknotes and 500 coins in one minute. The capacity is up to 30,000 banknotes and up to 5,000 coins with the possibility of increasing the capacity.

Security: according to the customer’s needs, it is possible to install an ATM safe of the second or first resistance class.

See the solution in operation: KorpOn, Asvio Bank, Doha Airport.

The network of automated deposit machines will ensure centralised deposit and collection. The main advantage is that financial institutions do not have to invest in hardware and software. They only pay a commission from each payment made on the device.

SECOND STEP – funds under the full supervision of two software products: RS Core and CAshLAB. What they can do:

- RS Core controls all transactions and payments, allowing to administer roles, branches, interfaces and generate reports, etc. It integrates seamlessly with both devices and bank accounting systems, making the necessary data available in one environment.

- CashLAB helps to manage cash flows: it monitors the balance sheet to ensure the required amount of funds for daily operations, optimises their use, forecasts income and expenses (including for liquidity purposes), informs about the state of fullness of cassettes and the optimal number of collections, etc.

The software allows one to optimise the operation of the CIT and avoid device downtime. It can be used in two formats: on the customer’s side, which administers the processes independently (In-House), or in the RENOME SMART cloud environment (Software as a Service). It can be easily integrated with the company’s necessary cash management software).

THIRD STEP – the CIT service receives an application for collection (notified by CashLAB) and delivers the cash to the cash centre, where a sorting table is located. The latter minimises the use of manual labour: just pour the banknotes out of the bag and get convenient stacks.

The RV5000 Sorting table is designed to process unsorted cash withdrawn from an automated deposit machine or during a retailer’s collection. It automates the process of forming stacks, allows you to keep track of crumpled bills or damaged units.

The key is that it processes 10 banknotes in less than a second, or 40% faster than manual processing.

FOURTH STEP – industrial banknote processing by a cash centre, where banknotes are counted at one time, and the number of errors and manual processes is minimised by introducing new equipment.

In a modern cash centre, automated banknote processing is used, where the results of counting and sorting are automatically transferred from the sorter to the cash centre management software. The continuous flow of cash is ensured by the available separation cards, and jams are eliminated without stopping the count. Reports and printed forms are generated automatically. The entire counting process works in synergy with the cash register equipment.

We suggest using the BSP C2 sorter for branches and cash centres with a 900-banknote receiver capacity and 1050 banknotes per minute; the BSP C5 sorter for cash centres with a 1500-unit receiver capacity and 25,000 banknotes per hour; and the BSP M3 industrial device with a 30,000-banknote per hour capacity.

“Our devices are designed for continuous operation, optimise staff costs by up to 30% and increase the cash centre’s throughput by 35%. In addition, they minimise the risk of human error and generate reports and printed forms automatically, which reduces the time required to process them.”

FIFTH STEP – perfect service. According to the RENOME SMART team, it includes not only the implementation phase, but also support, remote diagnostics, and consultations that reduce the frequency of engineer visits and equipment downtime. Our own network of qualified specialists throughout Ukraine allows us to meet high SLAs.

Instead of conclusions

Banks, collection services and financial companies used to spend resources on recounting and daily collections. Today, it is possible to process cash in large volumes more safely, efficiently and effectively.

By building an ecosystem of self-service devices for depositing revenue, you can accumulate funds and collect them at a convenient time. At the same time, participating companies will use fewer manual operations, personnel, and time. They will also be able to focus on improving the customer experience and their own development strategy.